Delisting shares under the proposed fixed-price mechanism could be a game changer, but retaining the 90% delisting threshold may derail its effectiveness, writes Freny Patel.

In line with global norms, India’s proposal to allow promoters the option to delist securities at a fixed offer price is likely to see a surge in the M&A activity of listed companies. It would also boost private investment in public equity (PIPE) transactions.

At least, that is the intention of the Indian capital market watchdog. Considering India’s emphasis on the “ease of doing business”, it is imperative that the Securities and Exchange Board of India (SEBI) ensures M&A deals remain straightforward.

The SEBI has proposed an alternative to the current reverse book-building method through the fixed-price delisting process, which brings Indian regulations closer to more mature markets. In the reverse book-building process, the shareholders decide the price at which they will sell their shares. Under the fixed-price method, the SEBI recommends giving the acquirer the option of providing an exit opportunity to public shareholders at a fixed price.

SEBI chair Madhabi Puri Buch has proposed revising the delisting mechanism because the watchdog does not want companies to be “trapped” inside the market. “The industry has been telling us that they have found certain problems under the current reverse book-building mechanism,” she says.

Commenting on the bids received under the current delisting mechanism, Buch says that sometimes there is a difference between an investor getting a fair value and extracting more value. “We need to balance out the requirements of both,” she told reporters.

The proposed new fixed-price mechanism should help facilitate the delisting of securities.

The industry has requested fixed-price delisting for years to help promoters organise the financing and better gauge market expectations, says Harsh Maggon, a Mumbai-based partner specialising in M&A and private equity transactions at Trilegal.

It is important to ensure that capital markets are conducive when it comes to facilitating exits, especially in the case of foreign shareholders, says Maggon.

The UK-based promoter of specialty chemicals company Ineos Styrolution opted to delist its India arm in 2020. Against an indicative offer price of INR480 (USD5.70) per share, the discovered price was INR1,100 per share according to the Delisting Regulations. Large institutional investors, which included mutual funds, tendered their shares in a price range of INR899 per share to as high as INR3,000 per share.

The UK parent company rejected the discovered price of INR1,100 per share and decided against making any counter-offer. Calling off its delisting plans, the Indian arm was subsequently sold to a strategic investor post-SEBI’s prescribed six-month cooling-off period.

Expectations and reality had not matched. With Ineos being a multibillion-dollar company, shareholders had expected that they could demand a higher price. But it is a fallacy of the reverse book-building process that the buyer has more money to give, say lawyers. In this case, despite being well-funded, the UK parent did not wish to allocate more funds to India.

The current reverse book-building process can be open to abuse by investors, a Mumbai-based lawyer says. Some “operators” have the tendency to mop up shares in a concerted effort to exceed 10% shareholding, thereby giving them the advantage to jack up the discovery price, which Buch said was “unsustainable”.

The current reverse book-building process allows an acquirer to make a counter offer should the discovery price not be acceptable. This is provided that the acquirer has managed to secure 90% of the shares, and the counter-offer cannot be lower than the book value of the company.

Under the proposed fixed-price delisting mechanism, the SEBI intends to lower the threshold requirement should an acquirer wish to make a counter offer. This is with the idea of ensuring the successful delisting of securities, depending on the ability of the promoters to garner more than 50% of the public shareholding.

In the event the delisting fails, there is a minimum cooling-off period of six months before an acquirer can attempt again to delist the securities.

Why do delistings fail?

Promoters or owners choose to voluntarily delist their companies to gain a greater degree of flexibility say lawyers citing various reasons including without having to seek shareholder approvals or to adhere to regulatory compliance warranted by listed companies. Some choose to delist if they feel the share price is not reflective of the company’s true value.

However, the delisting of securities under the current reverse book-building mechanism has seen more failures than successes. This is primarily because of an insufficient number of shares tendered and the price discovery being unacceptable to the promoters.

In a majority of cases, the reverse book-building process has failed due to high and unrealistic price expectations from investors, lawyers point out.

“The premium expectation for delisting needs to be reasonable, which is seldom the case,” says Abhishek Dadoo, a Mumbai-based partner specialising in public M&A at Khaitan & Co. Many a time, the purchaser may not have the financial resources tied up to offer a huge premium.

When a delisting proposal is announced, the share price often increases temporarily, creating false market expectations. This can lead to even higher delisting premiums. Typically, when a delisting attempt fails due to a high discovered price, the share price that was inflated during the process returns to its normal level.

Against the indicative delisting price of INR568, Universus Photo Imagings traded at INR396.60 on 15 September. It had touched a 52-week high of INR625 on 1 November 2022.

Unsurprisingly, given the confusion that surrounds it, delisting seldom ends in success, and as a result many financial sponsors and strategic investors tend to refrain from delisting their companies, Dadoo tells India Business Law Journal.

Vedanta’s delisting plans failed because one of the institutional investors, the state-owned Life Insurance Corporation of India, wanted a higher price of INR320 per share for its 6.37% shareholding, against the indicative delisting price of INR87.25.

LIC managing director Vipin Anand told the media at the time of Vedanta’s delisting proposal that INR320 was a fair price, and “we won’t tender Vedanta shares below fair value”. Vedanta did not have adequate funds to make a counter-offer and continues to be listed.

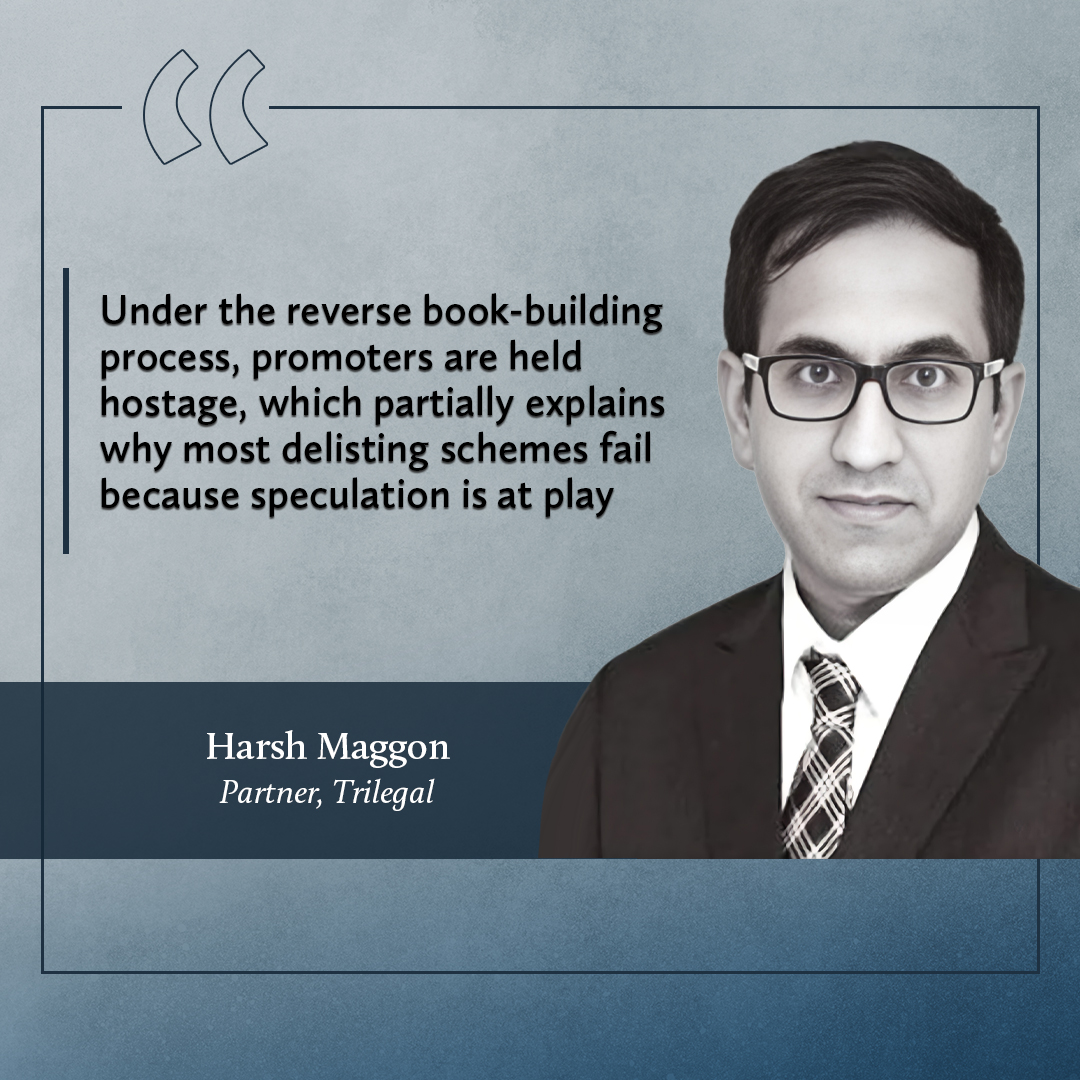

“Under the reverse book-building process, promoters are held hostage, which partially explains why most delisting schemes fail because speculation is at play,” says Maggon.

Certainty under fixed-price mechanism

The fixed-price delisting mechanism offers certainty to both shareholders and promoters and minimises price speculation by affluent investors.

While the reverse book-building process can be viewed as being more “democratic”, it tends to fail due to the non-alignment of price expectations. The fixed-price mechanism is expected to streamline the market. Large shareholders will not be in control nor be able to dictate prices, which will be decided by the promoters based on the SEBI formula.

The fixed-price delisting mechanism will eliminate subjectivity and prevent a small minority of shareholders from hijacking the delisting process to the disadvantage of the larger public shareholders who want an exit.

Dadoo says the option of choosing between the reverse book-building process and the fixed price mechanism provides greater flexibility to acquirers, although a large number of investors are likely to opt for the fixed-price delisting model.

“Delisting at a fixed price would limit the involvement of certain shareholders in driving up the delisting price,” says Rashmi Birmole, a Mumbai-based associate at Finsec Law Advisors. The SEBI’s proposal to allow the two mechanisms to co-exist enables acquirers to decide whether to go for reverse book-building or the fixed-price mechanism. However, the proposed fixed-price mechanism would be limited to those companies whose shares are frequently traded on the bourses in accordance with the SEBI’s Takeover Code.

The SEBI’s proposal to allow the two mechanisms to co-exist enables acquirers to decide whether to go for reverse book-building or the fixed-price mechanism. However, the proposed fixed-price mechanism would be limited to those companies whose shares are frequently traded on the bourses in accordance with the SEBI’s Takeover Code.

The delisting price under the fixed-price mechanism cannot be less than the floor price computed under the delisting regulations. The six-month cooling-off period continues to stand.

The SEBI’s proposal to set a floor price based on the adjusted book value of a company would ensure that none of the shareholders are short-changed, says Birmole. The minimum floor price will be linked to the adjusted book value of the company.

According to the SEBI Takeover Regulations, the floor price (minimum price for delisting) is based on the assumption that the company is going to remain listed. The SEBI proposes “adjusted book value” as an additional parameter for determining the floor price for delisted companies. It is intrinsically the net worth of the company, based on the asset’s fair market value.

Maggon agrees, saying that the adjusted book value is a good check on the market if the company is undervalued.

The concept of adjusted book value and how it is defined in the final regulations is bound to play a key role in determining the practical viability of a fixed-price delisting regime. For instance, certain companies may carry an extremely high adjusted book value, making the fixed-price delisting unviable. Ultimately, says Dadoo, the devil is in the details.

“If a company’s adjusted book value is much higher than its market price (or proposed fixed delisting price), then an acquirer may prefer the reverse book build process,” he says.

Likewise, the adjusted book value would be considered as a comparative metric by public shareholders in deciding whether or not to tender their shares, he adds.

The concept of fixed-price delisting already exists in India in the context of a combined open offer-cum-delisting under the takeover regulations.

On 28 September 2021, the SEBI amended the delisting framework to facilitate M&A transactions of listed companies by enabling acquirers to simultaneously launch open offers and an offer to delist the securities.

US private equity firm Blackstone launched an open offer for R Systems International at INR262 per share after its delisting attempt failed to garner adequate interest from public shareholders early this year. The company remains listed and is trading at INR507.

Open offer-cum-delisting is going to be an interesting space to watch, as is often the case in many overseas jurisdictions, says Maggon. Delisting would make stocks illiquid while open offers grant shareholders an exit option.

Although delisting is not sector-driven, many lawyers anticipate that companies in the infrastructure sector that are not too pleased about being under the watchful eye of the public may opt for delisting under the fixed-price mechanism.

“Listed companies have the added pressure of having to prove their performance and growth quarter-on-quarter,” says Maggon. “This may not always be possible for businesses with a long-term gestation period.”

Based on the SEBI’s Takeover Regulations, the open offer price needs to be at least the 60-day volume weighted average price. Since the acquirer wishes to delist the company, he says the fixed offer price would need to be at a premium.

Shareholders can tender their shares in either way. Should the delisting scheme fail because the acquirer is unable to achieve the requisite 90% threshold, then the shareholder still has the option to tender in the open offer, Maggon points out.

Lawyers agree that there are adequate checks and balances to ensure that the promoters do not abuse the system nor influence the decisions of the public shareholders.

Retail shareholders need not fear institutional shareholders having an upper hand with the fixed-price delisting mechanism, nor that companies can delist according to their whims. After all, the success of any delisting proposals requires the approval of the super majority of minority shareholders. Delisting challenges remain

Delisting challenges remain

Nonetheless, while the thorn in the reverse book-building delisting process may be removed under the new fixed-price mechanism, quite a few lawyers are sceptical.

“Implementing fixed-price delisting can be challenging due to differing views on pricing between public shareholders and promoters,” says Maggon, adding that the success of the delisting process is dependent on market forces.

Compared to most developed jurisdictions, India has the highest threshold of 90% when it comes to delisting, and it merely achieves illiquidity in a shareholder’s holdings, and does not squeeze out, he says.

Delisting under the proposed fixed-price mechanism will be a game-changer. However, as the 90% delisting threshold remains unchanged, the success or failure of the mechanism will largely depend on aligning market/shareholder expectations with those of the promoters intending to delist their companies.

Birmole agrees, saying that many delisting offers in the past failed partly because shareholders had not tendered their shares, possibly in expectation of a higher price. She says the alternate fixed-price delisting mechanism, which proposes to maintain the acceptance threshold at 90%, could continue to face difficulties in the delisting process should shareholders with substantial holdings choose against tendering their shares.

“Reducing the threshold from 90% to between 75-90% will enable promoters and acquirers to make counter-offers, which will increase the chances of success if a majority of the shareholders support the proposal,” says Birmole.

Lawyers agree that there are adequate checks and balances to ensure that the promoters do not abuse the system nor influence the decisions of the public shareholders.

Birmole says it is not the role of the SEBI to guarantee the success of every delisting offer. “The regulator’s prerogative has been to refine and rationalise the framework in order to facilitate delisting.”

At the end of the day, laws are useless if nobody uses them, which is why the SEBI’s chief is proactive and likes to bring about change for the development of the overall market. Laws do not change in a single step, Buch points out. Over time, big changes are often refined.