Since the Stock Exchange of Hong Kong Limited (HKEX), the preferred place for overseas listing of PRC domestic enterprises, revised the listing rules for the Main Board in 2018 and added three chapters such as Chapter 18A, more than 200 domestic enterprises have completed a Main Board listing on the HKEX. This article aims to provide domestic enterprises with reference for overseas listing by sorting out the basic paths to listing in Hong Kong and the compliance concerns of the HKEX.

Commerce & Finance Law Offices

Senior partner

Basic paths. (1) H-share issuance: The company to be listed is registered in mainland China, and involves the examination and approval procedures of the China Securities Regulatory Commission (CSRC). The CSRC has promulgated the Guidelines for Application for the “Full Circulation” of Domestic Unlisted Shares of H-share Companies, providing regulatory access. At present, some listed/to be listed H-share companies have applied for full circulation. (2) Red-chip listing (the “big red-chip listing” mode of a PRC domestic institutional holding is not included in this article): The company to be listed is registered outside mainland China, and its related business is operated in mainland China, which usually does not involve the examination and approval procedures of the CSRC, but involves the formalities of restructuring, foreign exchange and the commerce committee, etc. The examination and approval procedure is relatively simple, and the subsequent refinancing is convenient.

Commerce & Finance Law Offices

Partner

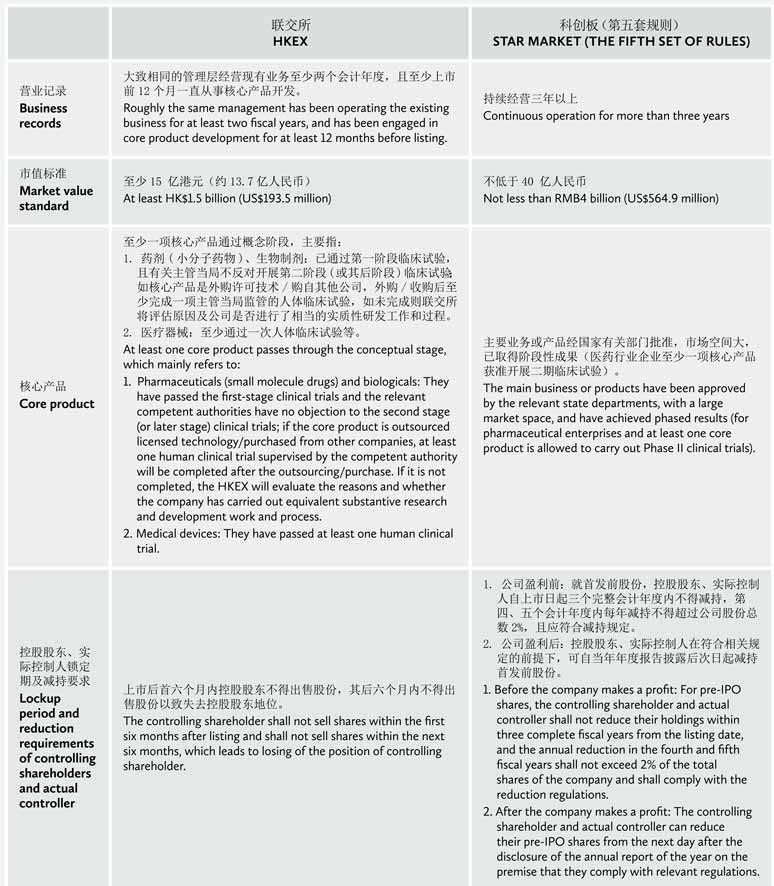

Comparison of listing conditions for biotechnology companies in Hong Kong and mainland China. Companies to be listed on the Main Board of the HKEX are generally required to meet one of these standards in the listing rules: “profit test”, “market value/income/cash flow test” and “market value/income test”. Chapter 18A has revised the listing conditions for biotechnology companies in terms of profit, market value and business records.

In Chapter 18A of the listing rules and the Guidance Letters (HKEX-GL92-18 and HKEX-GL85-16) of the HKEX, the comparable requirements on a number of listing conditions for biotechnology companies are lower than those for similar enterprises to list on the Shanghai Stock Exchange (SSE) Star Market, with the main differences as follows:

Compliance concerns of the HKEX. Taking into consideration listing precedents and relevant Guidance Letters (HKEX-GL63-13, HKEX-GL19-10, etc.), the HKEX pays attention to the legal compliance of enterprises in terms of entity qualification, business, taxation, intellectual property rights, property, labour and social security, litigation, arbitration and administrative punishment, and divides non-compliance events into three categories: major, systematic and non-important, and pays attention to the cause, nature, penalty/possible penalty, confirmation of competent authority, penalty rules and allowances, potential impact and remedies, etc. of major non-compliance events.

In practice, there are differences in the regulatory focus of compliance between the HKEX and domestic A-share regulators. For example, the confirmation forms of the competent authorities recognized by the HKEX are usually more flexible and diverse, but the integrity requirements and examination standards for the controlling shareholders/actual controllers are stricter.

Wang Bo is a senior partner at Commerce & Finance Law Offices. He can be contacted on +86 10 6569 3399 or by email at wangbo@tongshang.com

Chen Rui is a partner at Commerce & Finance Law Offices. She can be contacted on +86 10 6569 3399 or by email at chenrui@tongshang.com

")