Since the successful offering of the Qiyi Century Intellectual Property Supply Chain Financial Asset-Backed Security, China’s first intellectual property (IP) asset securitization product, at the end of 2018, a succession of IP securitization products with different types of underlying assets and transaction structures have seen the light of day. This article takes a brief look at the basic models of IP asset securitization in China, and the key legal points at present.

Basic models

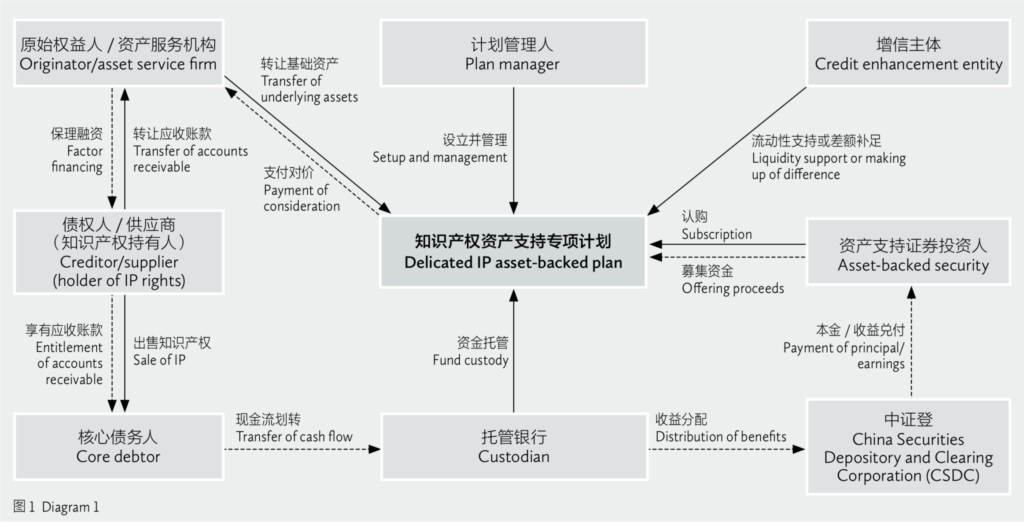

Supply chain model. In the IP supply chain trade, a supplier applies to a factor for financing using its accounts receivable claims against the core enterprise, and the factor acquires the accounts receivable claims and pays the transfer moneys. Subsequently, the factor transfers the accounts receivable claims, as the underly- ing assets, to the dedicated plan, and the dedicated plan pays the transfer money to the factor from the proceeds of the offering. The basic transaction structure is shown in diagram 1.

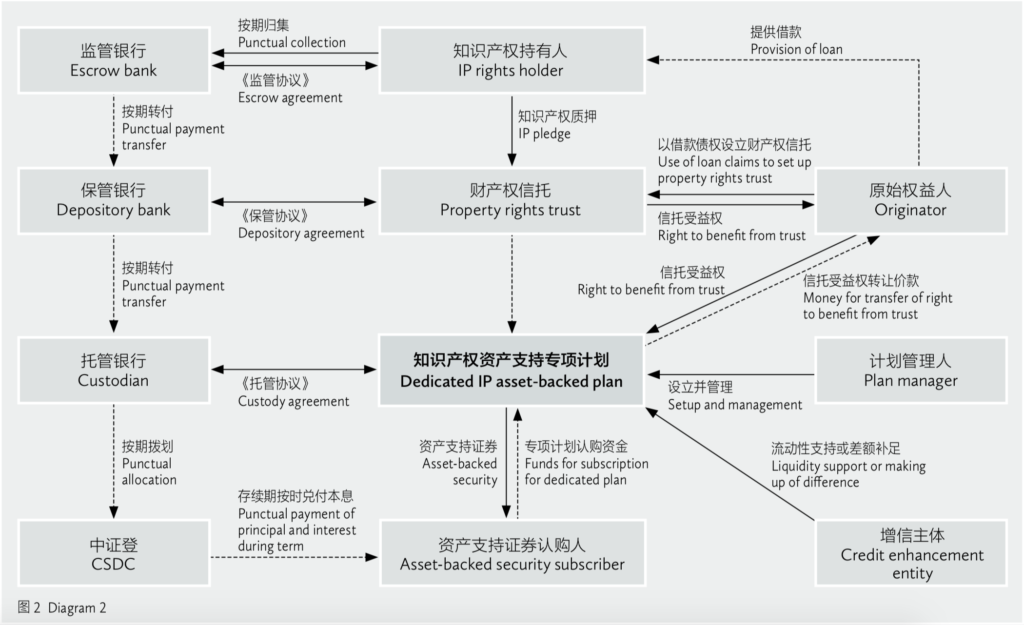

Quasi CMBS model. Referring to the structural logic of underlying CMBS (commercial mortgage-backed security) assets, the creditor provides a loan to the IP owner, the IP owner uses its IP to provide security in the form of a pledge for the claim, and the creditor, as originator, offers the asset-backed security. In practice, the dual special purpose vehicle (SPV) model, consisting of a property rights trust + dedicated plan, is generally used. The basic transaction structure is shown in diagram 2.

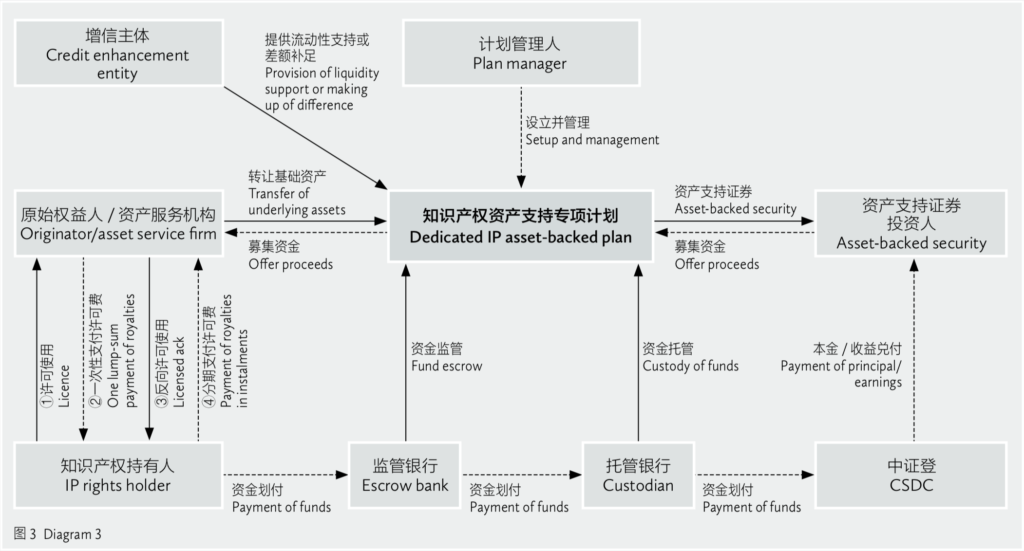

Secondary licence model. Once the owner of the IP licenses it to the originator, the originator pays a one- lump-sum royalty to the owner of the IP. The originator then licenses the IP back to the owner, and the royalties paid in instalments by the owner of the IP serve as the underlying assets to offer the asset-backed security. The basic transaction structure is shown in diagram 3.

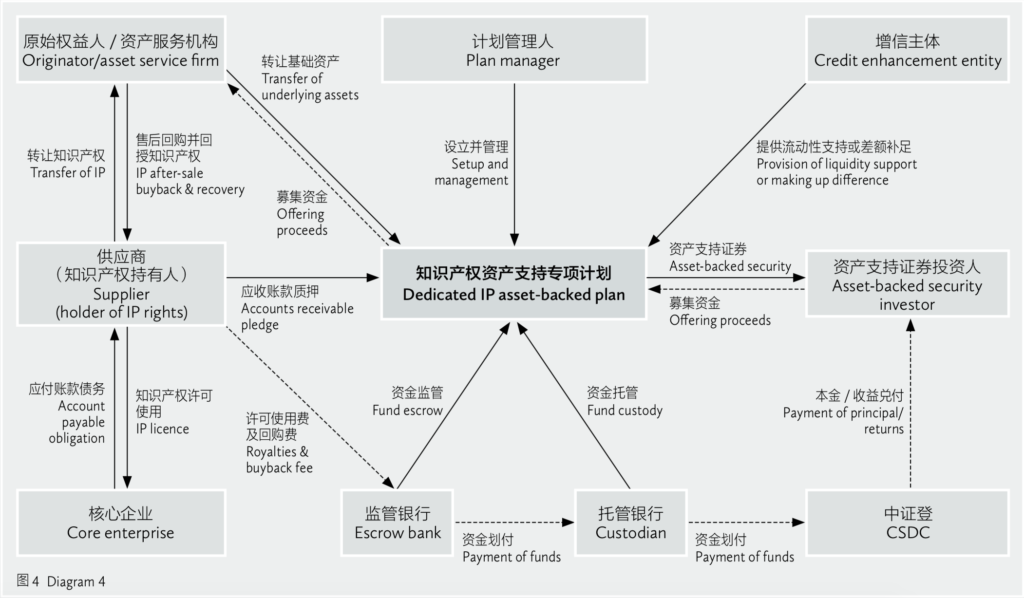

Supply chain + accounts receivable pledge + intellectual property buyback model. The IP owner transfers the IP to the originator and receives the transfer moneys in one lump sum. The originator then licenses the IP to the original IP owner, stipulating that the original IP owner pay royalties in instalments and buy back the IP at a nominal consideration once the licence term expires. During the licence term, the original IP owner further licenses the IP to the core enterprise, and the core enter- prise pays royalties to the original IP owner in instalments. Finally, the originator offers asset-backed securities using the royalties indirectly paid by the core enterprise as the underlying assets, and the original IP owner uses the royalties to provide security to the dedicated plan in the form of a pledge of accounts receivable. The transaction structure is shown in diagram 4.

Key points of law

Partner

Jingtian & Gongcheng

Definition of underlying assets.Due to the lack of constancy of the future operating income generated by relying solely on the IP, all of the assets under- lying IP asset securitization in China are IP derivative rights, e.g., IP royalty account receivable claims, IP pledge loan claims, IP financial leasing claims, etc. When carrying on IP asset securitization business, it is necessary to accurately define the legal substance of the underlying assets held by the originator, based on their type, and then determine the transaction structure and conduct precisely focused legal due diligence.

Creation of underlying asset pool.Since a single item of IP and its derivative rights are usually characterized as being of limited monetary value, having variable rights and being highly unstable, a number of similar intellectual properties or their derivative rights can, in order to enhance the stability of the underlying asset pool, expand the financing scale and enhance financing efficiency, and be combined to form an underlying asset pool so as to, on the one hand, satisfy the financing needs of multiple IP owners, and, on the other hand, reduce the investment risks associated with the as- set-backed securities through diversified purchase of underlying assets.

Associate

Jingtian & Gongcheng

Due diligence on, and confirmation of the rights in, the underlying assets. (1) Confirmation of the original acquisition of the IP. Regardless of whether the IP itself, or IP derivate rights, serve as the underlying assets, the lawful and valid acquisition of the IP is a prerequisite for IP asset securitization. Chinese laws and regulations stipulate different means for the acquisition of, and registration systems for, different types of IP, which should be applied accordingly when confirming the ownership of the IP.

Furthermore, if the original acquisition of the IP was completed abroad, it is recommended that a local law firm be engaged to issue a legal opinion on the lawfulness and validity of this original acquisition. If the IP is owned in common, it is recommended that a written document concerning the distribution and exercise of the rights among the owners be obtained during the legal due diligence, so as to avoid giving rise to a dispute, because certain owners lack the right to dispose of the IP, which would affect the stability of the underlying assets.

(2) Confirmation of IP secured by succession. If an entity involved in IP asset securitization business secures all or part of the rights in IP by way of succession, it is required to confirm the lawfulness and validity of the path by which the IP came into its possession. This needs to be confirmed during legal due diligence by reviewing the IP transfer contracts, licensing contracts, rights transfer registration documents, and proof of payment. Underlying assets where there are obvious defects in the transfer of IP-related rights should be removed from the underlying asset pool.

(3) Confirmation of IP derivative rights. Where IP asset securitization is carried out using accounts receivable claims and leasing claims as the underlying assets, and the stock exchange has issued guidelines for the confirmation of listing conditions, such guidelines will expressly provide for the qualifying criteria for such assets. For types of rights for which the stock exchange has not yet issued detailed rules, such as guidelines for the confirmation of listing conditions, these are required to be confirmed in accordance with the Administrative Provisions for the Asset Securitization Business of Securities Companies and Subsidiaries of Fund Management Companies, issued by the China Securities Regulatory Commission, and in light of the provisions of laws and regulations on the acquisition of the relevant rights.

Qin Maoxian is a partner and Zhang Dong is an associate at Jingtian & Gongcheng

Jingtian & Gongcheng

45/F, K. Wah Centre

1010 Huai Hai M. Road, Shanghai 200031, China

Tel: +86 21 2613 6212

Fax: +86 10 5809 1100

E-mail:

qin.maoxian@jingtian.com

zhang.dong@jingtian.com

www.jingtian.com

")