Hong Kong is proposing to allow listings of special purpose acquisition companies (SPACs) to catch up with its global counterparts.

The SAR’s biggest Asian competitor, Singapore, gained a head start by allowing SPAC listings on its bourse in early September.

Also known as blank-cheque companies, SPACs are shell companies that are formed to merge with a private company, helping them skip lengthy and expensive IPO processes.

The Hong Kong Exchanges and Clearing (HKEX) launched a 45-day public consultation of the planned SPAC listing regime, which ended at the end of October. There is still no timetable for an official launch.

On 3 September, the Singapore Exchange (SGX) relaxed listing rules to enable SPAC listing in the city, making it the first bourse in Asia. However, lawyers believe Singapore’s early start won’t significantly alter the competitive landscape between the two exchanges.

The ultra-low interest rates and money printing amid the covid-19 pandemic has driven a SPAC frenzy in the US since 2020. US SPACs raised USD98 billion in the first quarter of 2021, surpassing USD83 billion for the whole of 2020, according to Bloomberg. But the dealmaking has significantly slowed due to tightening oversight and fears of bubbles, plunging more than 86% to USD13.5 billion in the second quarter this year, the data show.

Nonetheless, Asian bourse operators are rushing to embrace the new model after an increasing number of well known Asian startups went public in the US. A total of 28 SPACs headquartered in Hong Kong and mainland China are listed in the US as of 15 October, raising USD4.2 billion, according to Law.asia’s SPAC research.

Meanwhile, two Hong Kong, eight mainland China and two Singapore companies have listed in the US via de-SPAC transactions in the past three years, with a combined market capitalisation of HKD26 billion (USD3.34 billion), according to the HKEX.

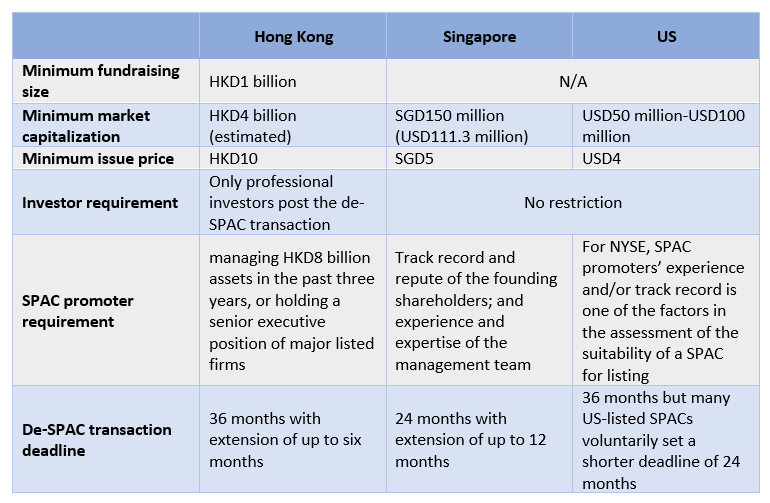

According to its consultation paper, Hong Kong’s proposed SPAC framework is much stricter than its global peers. Retail investors are not allowed to invest, and the key differences are as follows:

Simmons & Simmons

Hong Kong’s relatively conservative SPAC regime aims to attract large and high-quality SPACs and de-SPAC targets for Hong Kong listing, said Claudia Yiu, a Hong Kong-based partner at Simmons & Simmons. HKEX intends to uphold efforts to combat back-door listings and safeguard Hong Kong’s reputation and quality as a premier listing venue, keeping a higher standard of investor protection, she said.

“Hong Kong has a high ratio of retail investor participation in the stock market,” said Yiu. “Also, unlike other markets such as the US, where private litigation via class action is available as a means of check and balance, Hong Kong’s regulators tend to take up a more active role in investor protection.”

“The stringent SPAC regime intends to address various market concerns. The de-SPAC targets are required to fulfil the IPO listing requirements so that no sub-standard businesses and/or assets could make use of the SPAC regime to circumvent the traditional IPO listing requirements. The minimum fundraising size of HKD1 billion is a high threshold to allow only large and high-quality SPAC listings.”

Walkers

In contrast, there is no requirement of fundraising size for Singapore and the US SPACs, which raises doubts that it will make the bourse less competitive.

But Nicholas Davies, Hong Kong-based partner of corporate and investment funds group at Walkers, believes it is a sensible move to emphasise professional investment.

“The anticipated minimum fundraising size for HKEX SPACs is not off market with what we see in terms of the global SPAC market, with the average SPAC raising two or three times that amount,” said Davies.

“Under the current proposed rules, SPACs are unlikely to become mainstream as only a small number of players would meet the criteria. It will appeal to young growth companies,” he said.

Walkers

As SGX launched its SPAC regime, James Twigg, a partner at Walkers’ Singapore office, said he had seen considerable interest for SPAC listings in the city. The two exchanges were targeting different sectors, Twigg said.

“The HKEX has traditionally been the exchange of choice for Chinese companies,” he said. “Technology, media and telecom (TMT), healthcare and retail sectors have been the most active sectors for SPAC listings in the US, and we expect HKEX SPAC listings to follow a similar path.

“The SGX is dominated by mature local companies in traditional sectors. The Singapore government and the SGX will be hoping that the introduction of rules permitting SPAC listings will create new appeal as a destination for young, high-growth companies, particularly in the tech sector.”

Shearman & Sterling

Lorna Chen, Asia regional managing partner and head of Greater China at Shearman & Sterling, said it was unlikely that Asia’s IPO markets would change dramatically because of Singapore’s launch of SPAC listings. “Capital markets need many years to be nurtured and Hong Kong continues to be the best place for IPOs in the minds of Chinese companies.”

For Chinese companies seeking SPAC listings, Chen suggested they should focus on both domestic and overseas regulations.

“Apart from following any existing and new rules and guidance from mainland China’s regulators, sponsors from China need to know that other regulators, namely, the US Securities and Exchange Commission and the Financial Industry Regulatory Authority, have expressed increasing concerns over the use of SPACs in the US markets.”

")