The numbers of Chinese enterprises engaging in foreign investment has been increasing in recent years. This can be attributed to the central government’s “Going Out” strategy, which encourages domestic enterprises to invest in overseas expansion, and is also driven by the need for enterprises to globalize services.

Zhang Jida

达辉律师事务所

合伙人

Partner

DaHui Lawyers

Among the plethora of completed Chinese outbound investments, a significant number have been completed via an offshore legal structure. This issue briefly addresses the main types of offshore structures used by Chinese enterprises in outbound investment, together with their core characteristics and other matters that need to be considered.

Offshore structures

As the name suggests, an offshore structure refers to the legal framework or structure applicable in a particular offshore jurisdiction. This may include corporations, partnerships and trusts. As a matter of practicality, it is commonly understood that an offshore jurisdiction refers to one that provides a financial hub and acts as a tax haven for non-resident entities. Popular offshore jurisdictions include the Cayman Islands, British Virgin Islands (BVI), Bahamas, Bermuda and the Republic of Seychelles.

Key characteristics of offshore jurisdictions:

Tax benefits: For example, corporations registered and situated in such offshore jurisdictions will be exempt from taxes based on their revenues or profits. Instead, only a marginal amount of fixed management fees will be collected from businesses by the authorities, thereby significantly reducing their tax burdens.

Owen Yang

达辉律师事务所

合伙人

Partner

DaHui Lawyers

Confidentiality: Many offshore jurisdictions provide confidentiality protection with respect to the registered information of legal entities. For example, confidential information may include the beneficial owners of an entity (shareholders) and the shareholding structures. Such protection provides a high degree of commercial confidentiality.

Recognition: As a number of offshore jurisdictions were former British colonies, the legal systems are largely based on English common law. There are advantages in legal recognition and enforcement for companies registered in such offshore jurisdictions when conducting business or obtaining finance in common law jurisdictions such as the UK and the US.

Procedural advantages: The incorporation and associated procedures for corporations seeking registration in an offshore jurisdiction are simple and often require no regulatory authority’s approval as long as records are filed with the relevant authority. These procedural advantages provide flexibility to entities that are in the process of raising capital, restructuring or considering exit strategies.

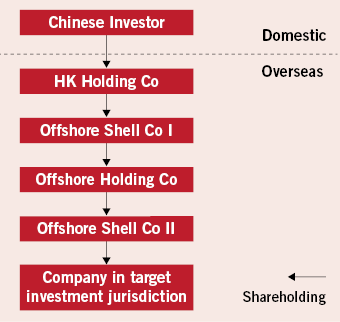

Common offshore structures

Common offshore structures

These are the commonly used offshore structures by Chinese enterprises in outbound investments:

The formation of a Hong Kong holding company is to obtain certain tax benefits between Hong Kong and mainland China. As a well-established financial hub for Asia, Hong Kong is a platform for outbound investment in facilitating funds settlement and engaging in foreign exchange transactions.

The general objective of setting up an offshore holding company is to enjoy the tax benefits in the offshore jurisdiction. For example, a corporation can park its profits in the offshore jurisdiction, which is usually a tax haven.

Generally speaking, the primary objective of the two offshore shell companies is to take advantage of the high degree of confidentiality protection offered in the offshore jurisdiction, which provide two cloaks of secrecy regarding investment information. Another objective is usually to leverage the procedural convenience in terms of company registration and change of ownership offered in the offshore jurisdiction. For example, with the offshore shell company exit strategies can be formulated without the sale of the offshore holding company, as the shares of the offshore shell company can be sold. Hence, this will not impact the investment activities of the offshore holding company.

Key considerations

Some key considerations when using offshore structures in outbound investments are as follows:

Choice of offshore jurisdiction: It is important to consider both the location of the investment and associated taxation matters in selecting the appropriate offshore jurisdiction. For example, for outbound investments targeted towards the UK and the US, the typical choice of offshore jurisdictions includes the Cayman Islands, BVI, Bermuda and other jurisdictions that are geographically and historically close to both countries. For outbound investments targeted towards Europe, relevant factors for determining the appropriate offshore jurisdiction include geographic location and tax benefits – the Republic of Malta being one such example.

Choice of entity: In offshore jurisdictions, the types of business entities available include companies, trusts and partnerships. The most common type of entity in an offshore structure is that of a company. This is due to considerations related to tax, asset control and liability. However, in practice there are also a number of trusts and partnerships being used in offshore jurisdictions in certain projects.

Filings and approvals: Depending on the circumstances of an outbound investment project, setting up or making changes to an entity in an offshore jurisdiction may require making filings and obtaining regulatory approvals in both jurisdictions. Investors should take such factors into consideration before embarking on any action.

Conclusion

As discussed above, appropriately using offshore structures can effectively: (i) reduce the investor’s tax burden; (ii) protect and shield confidential company information from the public; (iii) enhance legal recognition; and (iv) improve the prospects of overseas financing, restructuring and exit strategies. As the use of an offshore structure strategy involves navigating different legal jurisdictions and complex tax and compliance issues, it is recommended that investors always seek the advice of professionals.

北京市建国门外大街一号国贸大厦3720室

邮编:100004

Suite 3720, China World Tower

1 Jianguomen Outer Street

Beijing 100004 China

电话 Tel: +86 10 6535 5888

传真 Fax: +86 10 6535 5899

电子信箱 E-mail:

jida.zhang@DaHuiLawyers.com

owen.yang@DaHuiLawyers.com

www.dahuilawyers.com

")