State-owned assets (SOAs) play a dominant role in China’s economy, and state-owned enterprises (SOEs) are among the most important participants in Chinese overseas investments. The enhancement of an enterprise’s international competitiveness through overseas investments and acquisitions to maintain and increase the value of SOAs will become one of the reform directions for SOEs. This article focuses on the State-owned Assets Supervision and Administration Commission’s (SASAC) recently issued Measures for the Regulation of Overseas Investments by Enterprises under the Central Government (order No. 35), and analyzes the recent changes in regulating overseas investments with SOAs.

Partner

EY Chen & Co. Law Firm

Innovative regulation

SASAC formulates a negative list for offshore investments by enterprises under the central government (CGEs), determines the offshore investment projects that fall into the prohibited category and the special oversight category, divides the regulation of the offshore investment projects of CGEs into categories, specifies the baseline for the oversight of the investments of investors, and draws a red line for the investments of CGEs.

CGEs are prohibited from investing in all offshore investment projects included in the prohibited category of the negative list; for offshore investment projects included in the special oversight category of the negative list, CGEs are required to make submissions to the SASAC to carry out investor review and checking procedures; and for offshore investment projects not included, CGEs are free to decide based on their strategic development plans.

CGEs are the decision-making, execution and responsible entities for offshore investment projects. CGEs should formulate their own more stringent and specific offshore investment project negative lists on the basis of the SASAC negative list.

Order No. 35 defines certain key concepts. The term “main business” means the main business engaged in by a CGE as determined in its strategic development plan and confirmed by the SASAC; and non-main business means any business engaged in other than the main business. Overseas investments are high-risk and complex, and investments in main business are more conducive to the leveraging by an enterprise of its comparative advantages, enhancing the success rate.

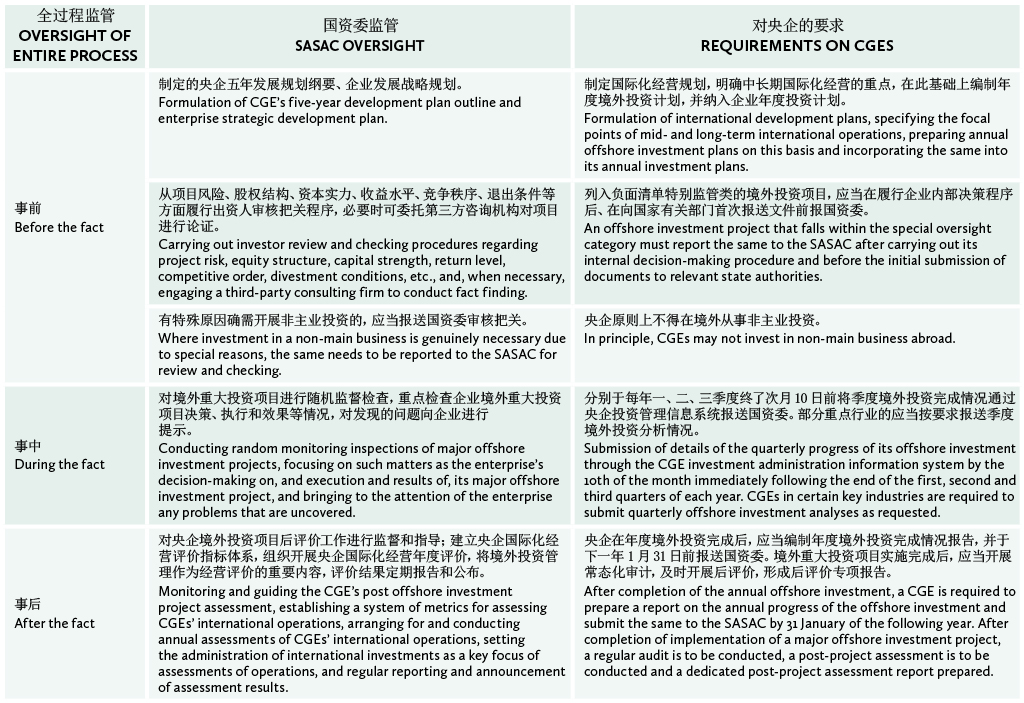

Oversight over entire process

Order No. 35 requires oversight over the entire investment process, placing equal emphasis on before-the-fact, during-the-fact and after-the-fact oversight. It emphasizes strengthening compliance before the fact, focusing on monitoring during the fact and strengthening accountability after the fact. Details are shown in the table on the next page.

Multifaceted oversight

Order No. 35 stresses development of the investment oversight system. Multifaceted oversight of the investment activities of enterprises is to be realized through the establishment of sound rules and regulations for the administration of investment, optimization of the investment administration information system, implementation of the investment project negative list, strengthening the linkage of investment and oversight, etc.

First, SASAC and the central government are required to enhance the level of computerization of information on the administration of offshore investment, carry out full coverage dynamic monitoring, analysis and administration of offshore investments and preemptively guard against the political, legal, social, safety and other such risks faced by CGEs in their offshore investments.

Second, the SASAC is to realize full coverage oversight of the offshore investment activities of CGEs and uncover at its own initiative investment risks through the establishment of a sound investment and oversight linkage mechanism and leveraging the co-ordination of such relevant oversight functions as strategic planning, legal compliance, financial monitoring, property title administration, assessment and distribution, capital application, cadre management, monitoring by external nominees to supervisory boards, and discipline inspection, etc.

Through order No. 35, the SASAC has continued the practice of formulating dedicated measures for regulating offshore investment. While essentially maintaining consistency between regulatory philosophy and regulatory methods on the one hand, and domestic measures on the other, it further emphasizes guidance by strategic plans, insists on focusing on the main business, and further emphasizes control of offshore risks and protection of the safety of offshore assets to safely escort the overseas investments of CGEs.

Lin Zhong is a partner at EY Chen & Co. Law Firm

中国上海市浦东新区世纪大道100号

上海环球金融中心51楼 邮编:200120

51/F, Shanghai World Financial Center

100 Century Avenue, Pudong New District

Shanghai 200120, China

电话 Tel: +86 21 6881 5499

传真 Fax: +86 21 6881 7393

电子信箱 E-mail:

zlin@eychenandco.com

www.eychenandco.com