The third board market, initially known as the share transfer system, officially opened on 16 July 2001. At the time, the “New Third Board” market referred to the pilot project where unlisted joint stock limited companies in Zhongguancun Science Park entered the share transfer system to carry out transfers.

中伦文德律师事务所

合伙人,信托与资产证券化专业委员会主任

Partner, Head of the firm’s Trust and Asset Securitisation Practice

Zhonglun W&D Law Firm

In 2012, expansion of the New Third Board was approved by the State Council. To the original pilot Zhongguancun Science Park were added the Shanghai Zhangjiang High-tech Industrial Development Zone, East Lake High-tech Zone and Tianjin Binhai Hi-tech Industrial Development Park.

On 11 October 2012, the China Securities Regulatory Commission (CSRC) formally issued the Measures for the Regulation of Unlisted Public Companies, which were followed by a series of complementary measures, or new regulations. On 16 January 2013, the National Equities Exchange and Quotations (NEEQ, or New Third Board) was established.

Executive meeting

On 6 May 2013, Premier Li Keqiang presided over an executive meeting of the State Council, where it was stated that a plan to expand the scope of the NEEQ pilot project was to be issued. According to reports, the CSRC is currently studying the formulation of a specific plan to expand the New Third Board pilot project to the entire country.

Construction of the new technical system will be completed by around November this year, and after connection testing and simulated transactions, will formally come online before the end of the year. At that time, in addition to such functions as share quotes, transfers, targeted financing, etc., the NEEQ will permit the transaction of such new products as bonds.

The New Third Board has the following particular advantages:

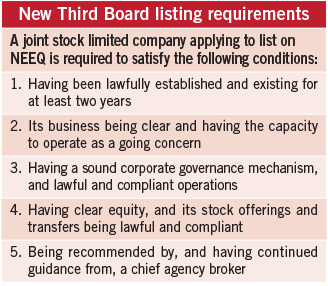

As the objective of the New Third Board is to foster new small- and medium-sized enterprises, the listing threshold is low. No financial targets are set in the listing conditions, it does not require “prominence in main business”, and companies are not restricted to high-tech firms.

Multi-channel

The New Third Board permits companies applying for listing to make targeted offerings, or carry out targeted financing at the same time they apply for listing, and actively broadens the financing and refinancing channels for listed small- and medium-sized enterprises.

The Third Board has established a small financing waiver system and price quote offering system. Once approval is secured, an offering may be made in multiple tranches without additional approvals. This permits listed enterprises to carry out refinancing through such means as transfer on the open market, convertible bonds, private bond offerings and other securities products, in addition to targeted capital increases.

High efficiency

The abundance of trading rules for the third board market is conducive to enhancing the market’s trading efficiency via:

- implementation of a market maker system, and additional transfer methods;

- optimisation of the transfer by agreement method, and provision of centralised bidding and transfer services;

- no limits on the price range for stock transfers;

- transfer information that is to be public and transparent, and it is specified that such transfer information as share transfer real-time data, public information on stock transfers, etc. is to be posted by NEEQ every trading day, and an index is to be prepared as required.

Back to market principles

The New Third Board returns to market principles, with adherence to the principle of guidance by the market in listing reviews. Securing of a government letter of confirmation is no longer a necessary condition for an enterprise to list. With respect to the development features and risk features of innovative and venture small- and medium-sized enterprises, market principles are adhered to in listing reviews. The New Third Board implements a regulatory system that combines self-regulation and outside regulation. First, self-regulation of the chief agency brokers, listed companies, investors and other intermediary firms is implemented by NEEQ, and it is additionally subject to centralised regulation by the CSRC on the foundation of the former; and added are measures to suspend and lift restrictions on the sale of shares by the controlling shareholders and actual controllers of listed companies, as well as the disciplinary sanction of recording acts of bad faith in the securities and futures market integrity file database.

Sound divestment mechanism

The new regulations establish a mechanism for transfers between the New Third Board and the floor trading market. Pursuant to the new regulations, where an enterprise listed on the New Third Board fully satisfies the conditions for listing on the Shanghai or Shenzhen stock exchanges, it may directly apply for listing to the exchange. This is in substance a provision of principle of a “listing by introduction” model of mature markets.

The New Third Board has become a new divestment method for private equity/venture capital (PE/VC) investments. The New Third Board displays numerous companies that operate in a compliant manner and that have a certain competitiveness and technical content, providing PE/VC with a platform for seeking quality projects. In 2012, the New Third Board had 23 listed enterprises that made targeted capital increases, for a financing amount of about RMB900 million (US$146.5 million). Of the new shareholders that participated in the targeted capital increases, 60% were PE/VC.

The New Third Board has become a new divestment method for private equity/venture capital (PE/VC) investments. The New Third Board displays numerous companies that operate in a compliant manner and that have a certain competitiveness and technical content, providing PE/VC with a platform for seeking quality projects. In 2012, the New Third Board had 23 listed enterprises that made targeted capital increases, for a financing amount of about RMB900 million (US$146.5 million). Of the new shareholders that participated in the targeted capital increases, 60% were PE/VC.

New platform

The above-mentioned features and advantages of the New Third Board have enabled it to become a new platform in China’s capital markets. Under the current environment, characterised by a weaker economy, particularly under current conditions where IPO approvals have been curtailed, the New Third Board will undoubtedly become a more attractive investment and financing option for such market entities as China’s small and medium-sized enterprises and PE/VC.

Cao Chunfen is a partner at Zhonglun W&D Law Firm and head of the firm’s Trust and Asset Securitisation Practice

北京市朝阳区西坝河南路1号

金泰大厦19层

邮编:100028

19/F, Golden Tower

1 Xibahe South Road, Chaoyang District

Beijing, 100028, China

电话 Tel:+86 10 6440 2232

传真 Fax:+86 10 6440 2915/2925

电子邮箱 E-mail:

caochunfen@zlwd.com

www.zhonglunwende.com

")