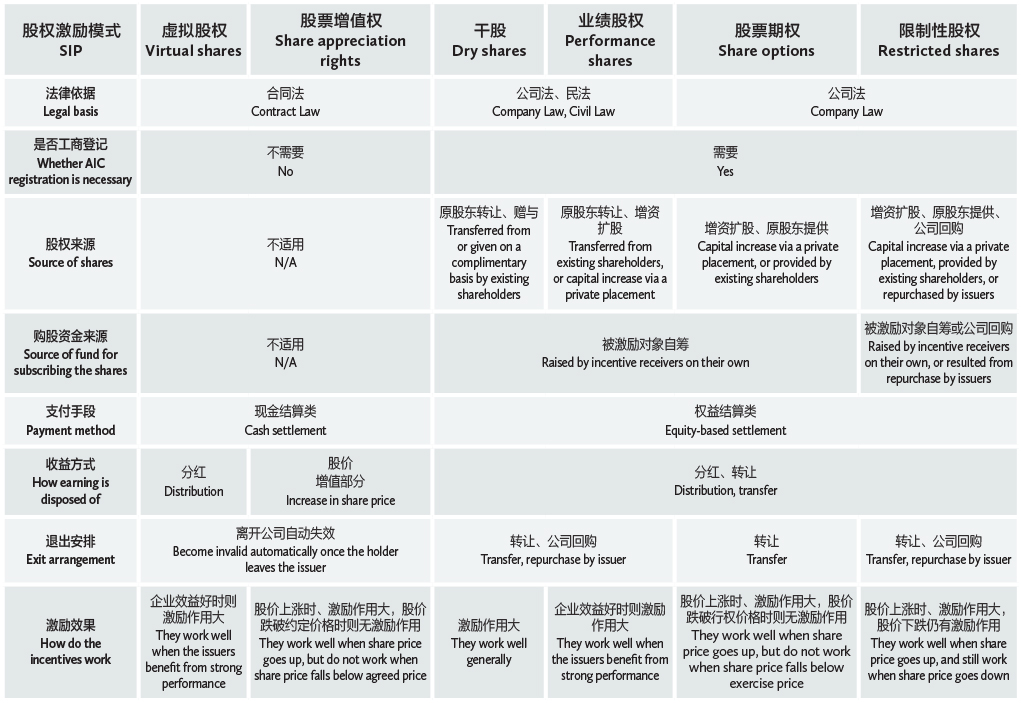

Non-public companies benefit from ample flexibility in designing their share incentive plans due to the lack of pertinent legal and regulatory provisions in China governing equity incentives provided by non-public companies. In accordance with the Circular of the Ministry of Finance and the State Administration of Taxation on Improving the Income Tax Policies for Equity Incentives and Technology Investments, generally there are three categories of underlying securities from which non-public companies may choose for their share incentive plans (SIPs), namely, restricted shares, share options and shares. In practice, equity incentives are provided especially in forms that include virtual shares, share appreciation rights, free shares (also known as “dry” shares), performance shares, share options and restricted shares. Below is a table that provides a comparative overview of these equity incentives.

JIANG FENGTAO

恒都律师事务所创始合伙人

Founding Partner

Hengdu Law Firm

A snapshot of features of non-public companies’ SIPs. Although there is not any well-established legal framework for SIPs of non-public companies, they can design and operate their SIPs with reference to laws and regulations applicable to public companies as well as their SIPs. SIPs of non-public companies have the following features compared with those of public companies.

How incentives are provided. Public companies generally provide equity incentives by issuing share options, restricted shares and other appropriate securities, while non-public companies benefit from more flexibility that enables them to provide more diversified incentives, which include but are not limited to share appreciation rights, virtual shares and performance shares.

Source of shares. The shares provided by public companies as incentives are transferred from existing shareholders, who first transfer the shares to the companies, from which the shares are subsequently granted to incentive receivers. Alternatively, public companies may issue shares to incentive receivers through private placement. As another solution, public companies may repurchase shares from the secondary market and then grant them to incentive receivers within one year. The shares provided by a non-public limited liability company as incentives are transferred from its largest or controlling shareholder, or result from capital increase through private placement to incentive receivers. For a non-public joint-stock company, in order to get shares to be provided as incentives, it needs to repurchase shares or cause transfer of shares, or it may launch a private placement to incentive receivers.

ZHENG MIN

恒都律师事务所资本市场高级律师

Senior Capital Market Associate

Hengdu Law Firm

Number of incentive receivers. Given their public nature, public companies are not bound by any restrictions regarding the number of shareholders. For a non-public company, it must restrict the number of its shareholders to 50 in the case of a limited liability company or to 200 in the case of a joint-stock company. That is why SIPs of non-public companies generally restrict eligible incentive receivers to a certain number of people, comprising mostly of officers and crucial professionals. There are also many that provide incentives by utilizing shareholding vehicles, nominee shareholders or trusts, which may pose legal obstacles to companies’ paths to IPO.

How excise price is fixed. The exercise price of options issued by a public company is typically based on the price of the company’s shares on the secondary market at the time of conclusion of the option agreements. However, in the case of non-public companies without open market price, generally exercise price is fixed particularly based on financial indicators,

taking into account the practices of comparable industry peers.

Varied effects of SIPs. SIPs work well for public companies because incentive receivers have opportunities to cash in their incentives on the secondary market, given the fact that the companies’ shares are traded on open markets. They may fail to achieve the same effect with non-public companies, because equity receivers are unable to take some money off the table by selling their illiquid shares through open markets. When non-public companies perform well, however, their SIPs do work.

Anyway, an effective SIP helps with motivating staff members and developing core competitiveness for companies. It can drive better alignment between company members and officers so that they join hands to enable sustainable growth of non-public companies.

Jiang Fengtao is the founding partner and Zheng Min is a senior capital market associate at Hengdu Law Firm

![]() 北京市朝阳区建国门外大街1号

北京市朝阳区建国门外大街1号

国贸大厦3期B座50层 邮编:100004

50/F, Block B, China World Trade Center Tower 3

No.1 Jian Guo Men Wai Avenue

Chaoyang District, Beijing 100004, China

电话 Tel: +86 10 5985 2999

传真 Fax: +86 10 5760 0599

电子邮箱 E-mail:

hengdulaw@hengdulaw.com

")

")