For 20 years, e-signatures and the transformation to paperless offices were dangled as the promises of a brave new world that remained, well, on paper. Now a tectonic shift is underway. Georgy Thomas reports

From July through to early September of 2021, shares of Nasdaq-listed DocuSign hit all-time highs on multiple trading sessions, valuing the loss-making company at over USD60 billion (MCap) – an astonishing 34 times its trailing 12 month (TTM) revenues. The e-signature (electronic signature) software maker was a market darling, among the biggest beneficiaries of the shift to remote work during the pandemic.

Today, the stock is down 80% from its peak thanks to several missteps in execution and an inability to close sales deals. But no one’s suggesting that companies around the world would head back to paper-pushing with a vengeance.

In a sense, DocuSign’s all-time high share prices signalled a coming of age for e-signatures and digital signatures. The company was set up in 2003, a few years after the legal framework around e-signatures emerged globally. There was the EU’s Electronic Signature Directive of 1999, while the US had the Uniform Electronic Transactions Act in 1999, and the Electronic Signatures in Global and National Commerce Act (E-sign Act) in 2000.

Also in 2000, India enacted its Information Technology Act (IT Act). UNCITRAL, a UN body, published its Model Law on Electronic Commerce in 1996, and the Model Law on Electronic Signatures in 2001 – both were hugely influential. But the market took its time to mature. It was the jolt from the pandemic that made the world sit up and notice that e-signatures had finally arrived.

India Business Law Journal spoke to five experts drawn from industry and law about the new dawn in the e-signature market. All were unanimous that the pandemic was a positive for e-signatures. “The onset of the pandemic did see a surge in demand,” says Archana Balasubramanian, founding partner at Agama Law Associates in Mumbai. “To support their remote workforces in 2020, businesses had no choice but to digitise their former procedures.”

India Business Law Journal spoke to five experts drawn from industry and law about the new dawn in the e-signature market. All were unanimous that the pandemic was a positive for e-signatures. “The onset of the pandemic did see a surge in demand,” says Archana Balasubramanian, founding partner at Agama Law Associates in Mumbai. “To support their remote workforces in 2020, businesses had no choice but to digitise their former procedures.”

Biju Varghese in Bengaluru, who is senior vice president and head (India and APAC) of global strategic alliances at eMudhra, a certifying authority for digital certificates licensed by the government, says: “Covid in many ways made institutions and individuals realise that e-signatures are not only a matter of efficiency, but also play a crucial role in business continuity.”

Shreya Suri, a partner at IndusLaw in New Delhi, agrees. “There was a particular spike in the popularity of digital signatures/e-signatures during the pandemic and the upward trend has continued.”

GROWTH DRIVERS IN A SUNRISE MARKET

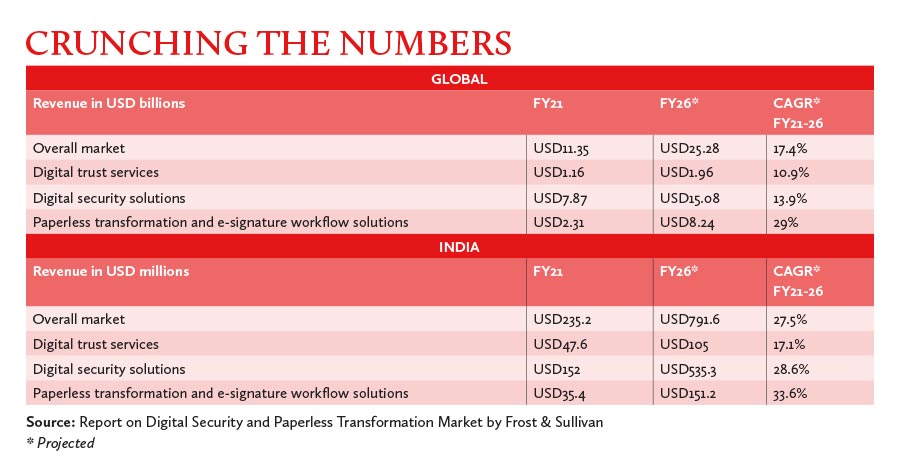

The digital security and paperless transformation market – which e-signatures are a part of – has been growing in double digits globally since 2016, and in India, too (see Crunching the numbers). The global market was valued at USD11.3 billion as of 2021. In India, it was worth INR18.6 billion (USD233 million). The market is projected to grow at a compound annual growth rate (CAGR) of 17.4% globally, and 27.5% in India by 2026.

Again, of its three verticals, the growth driver is paperless transformation, which is entirely about managing e-signature workflows. It’s surging ahead, projected to grow at a CAGR of 29% globally, and 33.6% in India, by 2026. But the story doesn’t end there. The digital signature component of the other two verticals – digital trust services and digital security solutions (see Under the hood) – are outpacing peer elements in growth, both globally and in India.

You must be a

subscribersubscribersubscribersubscriber

to read this content, please

subscribesubscribesubscribesubscribe

today.

For group subscribers, please click here to access.

Interested in group subscription? Please contact us.