Q : What types of asset securitisation are there?

A: There are three main types of operable asset securitisation in China: credit asset-backed securitisation (credit ABS), under the purview of the central bank and the China Banking Regulatory Commission; corporate asset-backed securitisation (corporate ABS) under the purview of the China Securities Regulatory Commission (CSRC); and asset-backed notes (ABNs) under the purview of the National Association of Financial Market Institutional Investors. These types of securitisation have taken form mainly in line with the way in which the administration of the financial industry in China is divided.

Lu Qunwei

安杰律师事务所

合伙人

Partner

AnJie Law Firm

At present, however, the underlying assets for ABNs are not sold to special purpose vehicles (SPVs) to achieve complete separation from the issuer, and strictly speaking are not asset-backed securitisation, but rather more like asset mortgage-backed securities.

Q: What are the core legal issues in asset securitisation?

A: Asset securitisation is preconditioned on the existence of claims or beneficiary rights, and is the process by which claims or beneficiary rights are gradually capitalised; its objective is the realisation of a transformation from borrower credit to asset credit and it has two core legal issues:

- Genuine asset sale and bankruptcy remoteness. The core of asset securitisation is the separation of the assets to be securitised from any bankruptcy of the original rights holder. In the transaction structure for asset securitisation, an SPV must be brought in, with the original rights holder making a genuine sale of the assets to the SPV, and the SPV, as the entity, then offering the securities. If a genuine sale of the underlying assets is not realised through an SPV, the securities can, at most, be called asset mortgage-backed securities.

To achieve complete bankruptcy remoteness, the selection and design of the legal form of the SPV is of utmost importance. Legal forms such as limited liability company, limited partnership, etc., have greater financial independence when compared with dedicated asset management plans and pooled fund trust plans, although the latter two forms are now the most commonly used for SPVs in China. This is mainly due to considerations of tax and regulatory convenience.

戴志文

Jeremy Dai

安杰律师事务所

合伙人

Partner

AnJie Law Firm - Asset selection and structuring of asset pool. In addition to being able to generate a stable and predictable cash flow, the assets that are to be securitised must have the features that permit them be securitised. If structuring of an asset pool is required, the assets additionally need to be homogeneous. The underlying assets for credit ABS are relatively easy to determine and select.

The selection of the underlying assets for corporate ABS is relatively complex because its scope is relatively broad and there aren’t an overly large number of restrictions. Pursuant to the Administrative Provisions for the Asset Securitisation Business of Securities Companies, the underlying assets for corporate ABS may be such property rights as the enterprise’s receivables, credit assets, right to benefit from a trust, right to benefit from infrastructure, etc., or immovable property such as commercial property, etc., or other property or property rights recognised by the CSRC. As a result, there is a greater range of choice for the underlying assets for corporate ABS, giving lawyers and other professionals greater innovative space in the determination of the assets available for securitisation and the design of the transaction structure.

Q: What new developmental trends are there in asset securitisation?

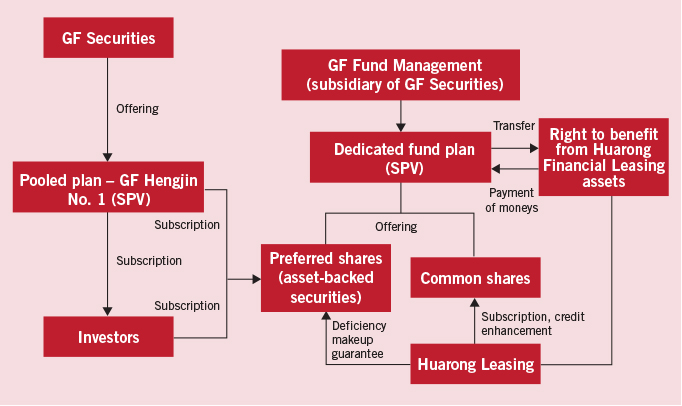

A: Since liberalisation of the corporate ABS business by the CSRC, the new developmental trends are: i) a huge increase in the number of applications and an increase in the speed of approvals; ii) an increase in the types of underlying assets, and the occasional appearance of new forms of asset pool; iii) a trend toward complex designs for the transaction structures that are no longer limited to the traditional structural models; and iv) the appearance of innovative models that circumvent the approval procedures. For example, the Huarong Financial Leasing asset securitisation product successfully circumvented the CSRC’s approval and regulation of corporate ABS products by virtue of a “dual SPV” model (for the structure, see the graphic).

Dedicated asset management plans require the approval of the CSRC, whereas pooled plans and dedicated fund plans are subject to the recordal system. Accordingly, it appears as if the dual SPV model is “rejecting what is near at hand to seek what is far away”, but it nevertheless successfully avoids the approval procedure. The dual SPV structure can also draw on the broad investment scope of dedicated fund plans to directly acquire “non-standard” underlying assets, thus also indirectly broadening the scope of underlying assets, something that a securities broker asset management plan or trust plan cannot do. The disadvantage of the dual SPV structure lies in the underlying assets being unable to cut their connection to Huarong Leasing, thus it is not asset securitisation in the strict sense of the word, but this does not detract from its innovativeness and feasibility, and it also provides more ideas for those involved in the industry.

![]()

北京市朝阳区建国门外大街甲6号

中环世贸中心D座26层

26/F, Tower D, Central International Trade Center

6A Jianguomenwai Avenue

Chaoyang District, Beijing, China

邮编 Postal code: 100022

电话 Tel: +86 10 8567 5988

传真 Fax: +86 10 8567 5999

www.anjielaw.com

电子信箱 E-mail:

jeremydai@anjielaw.com

luqunwei@anjielaw.com

")

")

")

")