The private equity market in Japan is very active, with trends indicating the Cayman Islands is a primary conduit for activity

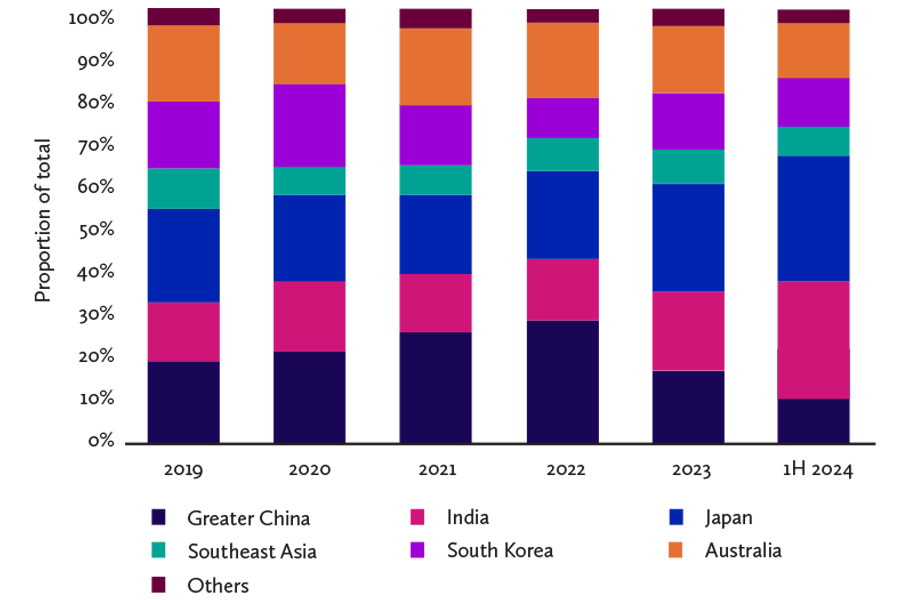

Japan has been the largest and most active private equity (PE) market in the Asia-Pacific since 2023 (see chart). PE-related deal making in Japan jumped last year as an ample supply of targets, low interest rates, a weaker yen and improved corporate governance helped Japan buck the trend to make the country the only market in APAC to see growth in 2023, and dealmakers anticipate a busy pipeline ahead.

Private equity-backed buyout deals in APAC by location

Source: Preqin Pro

Partner

Maples Group

Hong Kong

Tel: +852 9023 0037

Email: sharon.yap@maples.com

There are a growing number of investors chasing deals in Japan. The number of general partners (GPs) with a Japan office and a latest buyout/turnaround fund worth at least JPY50 billion (USD336 million) has doubled between 2012 and 2024. There are also many foreign investors not yet in Japan showing clear interest to be more active. Additionally, PE is also a preferred strategy of large Japanese limited partners (LPs).

Fundraising for buyouts in Japan defied the global trend of peaking in 2021 and then declining since. Instead, Japan buyout funds raised USD4.6 billion in 2023, three times the 2022 total. The fundraising streak has continued in 2024, with Japan leading the way for Asia ex-RMB denominated funds in the second quarter of 2024.

Advantages of Cayman Islands

When fundraising, it is important to use a reputable, well-established investment fund jurisdiction that LPs are familiar with. The Cayman Islands is the leading jurisdiction for offshore investment funds, attracting about 80% of all new offshore fund formations globally.

The Cayman Islands is at the forefront of the investment funds industry because of advantages including:

- Investor familiarity – a vital consideration when fundraising;

- Tax neutrality;

- Expertise in investment funds and experienced professional service providers;

- Economic and political stability;

- Commercial and flexible legislation;

- Well established, respected and sophisticated legal system;

- No exchange control restrictions; and

- The Cayman Islands is on the OECD white list.

Japan’s investment in Caymans

The Cayman Islands is the jurisdiction of choice for Japanese GPs and LPs investing in overseas investment funds, currently attracting more than two-thirds (67.3%) of such investment. At the end of 2022, Japanese holdings in Cayman Islands investment funds amounted to JPY87.6 trillion.

Use of ELPs for PE funds

The Cayman Islands offer a range of vehicles that could be used to structure an investment fund, including the exempted limited partnership (ELP), the unit trust, the exempted company, the limited liability company and the segregated portfolio company. The choice of structure is largely driven by the needs of the particular investment fund and its investors.

The ELP is widely used globally to structure PE funds, including funds that have been established for in-bound investment into Japan, and outbound investment. The ELP structure is commonly used to admit both Japanese and global LPs. Depending on the size and requirements of the PE fund, and the composition of LPs, more than one ELP may be formed to act as parallel funds or feeder funds – it is not uncommon to form an ELP solely for Japanese investors and another ELP solely for non-Japanese investors – and further ELPs may also be formed to act as co-investment vehicles for certain LPs.

The ELP is ideally suited for use in a PE fund context where contractual flexibility and tax transparency are often key considerations.

The ELP is a contractual arrangement between the GP who conducts the business of the ELP and the passive investor LPs. The development of Cayman Islands laws governing the ELP have been guided by the demands of the PE industry and are generally permissive and allow for contractual freedom.

The contractual nature of the ELP provides sufficient flexibility to accommodate all the typical provisions commonly negotiated between GPs and LPs, such as: the provision of side letter arrangements to select LPs, and all the key terms of PE funds including capital commitment and capital call arrangements; excuse provisions and default provisions; investor allocations and distributions; carried interest waterfalls; catch-up provisions and other fee arrangements; LP advisory committee provisions; and key man terms, among others.

A key man clause prohibits an investment firm or fund manager from making new investments if one or more key persons are not available to devote the necessary time to the investment. It is often included in fund or manager documents in the Cayman Islands.

An ELP is not an entity distinct from its partners and has no separate legal personality of its own.

Having no legal personality of its own, the ELP is generally regarded as being tax transparent (or as having tax “flow-through” status) for domestic tax purposes, including in Japan. LPs of an ELP enjoy the protection of limited liability and are not liable for the debts and obligations of their ELP as long as they do not take part in the conduct of the business of the ELP with persons who are not partners of the ELP.

The GP of an ELP is typically established as a special purpose vehicle (SPV), which has the advantage of insulating the investment manager from the GP’s liability for the ELP’s debts and obligations in the event the assets of the ELP are insufficient.

The GP SPV is typically established and controlled by the investment manager, permitting the investment manager to manage the PE fund without the need to involve a third-party operator. The GP SPV is often established as a Cayman Islands exempted company but may also be a foreign company, such as a Japanese company

26th Floor, Central Plaza

18 Harbour Road

Wanchai

Hong Kong

Tel: +852 2522 9333

Fax: +852 2537 2955

www.maples.com